The SEC’s Office of Investor Education and Assistance is issuing this Investor Bulletin to educate investors about target date funds. This Investor Bulletin discusses only target date funds that are mutual funds or exchange-traded funds (ETFs) registered under the Investment Company Act of 1940.

What are target date funds?

Target date funds are investment funds that hold a mix of investments, such as stock, bond, and other investment funds. They are designed to make investing for retirement or other goals more convenient by spreading your money among different investments (diversification) and by changing the investment mix or asset allocation over time.

The year in the name of a target date fund typically refers to the fund’s target date. For target date retirement funds, this date would be the year you expect to retire. For example, a fund called “Lifecycle 2060 Fund″ would be designed for individuals who intend to retire in or near the year 2060.

Target date funds are often structured as mutual funds or exchange-traded funds (ETFs), both of which are regulated by the SEC. But some target date funds that are held within retirement accounts are structured as collective investment trusts (CITs), which are not regulated by the SEC.

How are target date funds similar to other mutual funds and ETFs?

Like other mutual funds and ETFs:

- Target date funds offer people a way to pool their money in a fund that invests in various investments.

- The combined securities and other assets the fund owns are known as its investment portfolio, which is managed by an SEC-registered investment adviser.

- Fund investors receive an interest in the investment portfolio. This means each fund share represents an investor’s proportionate ownership of the fund’s investment portfolio and the returns the portfolio generates.

- Many target date funds are investment companies registered with the SEC. SEC registration requires the funds to provide ongoing disclosures and information to investors, among other things. It also provides other protections for investors, such as limits on illiquid or hard-to-sell investments in a fund’s portfolio and restrictions on a fund’s borrowings and debt.

- Target date funds can be held in different types of investment accounts, such as retirement accounts like 401(k)s or IRAs, college savings accounts, brokerage accounts, and others.

How are target date funds different from other mutual funds or ETFs?

Unlike other mutual funds and ETFs, target date funds rebalance or change the fund’s mix of investments over time in a way that is typically intended to become more conservative as you approach the target date. That means that the investment adviser typically shifts the fund’s investment mix from being more heavily focused on stocks (generally a higher risk of loss) in the beginning to being more weighted toward bonds (generally a lower risk of loss) as the target date nears.

Why is this important? When making investing decisions, investors consider the risk they are willing to take. Typically the potential for profit (or higher return) comes with a greater chance of losing money (or risk). The longer investors have to invest, the more risk they can generally afford to take because their investments have more time to recover from market dips. This means that as a retirement or other goal gets closer, investors typically will want less risky investments.

In a target date fund, the fund’s investment adviser typically takes care of shifting the investments from higher return (and higher risk) to lower return (but lower risk) as the target date approaches. In this way investors may be more prepared for their retirement or other goal without spending a lot of time shifting the mix of investments around themselves.

How does a target date fund work?

A target date fund is typically a fund of funds. That means the fund’s investment portfolio is made up of shares of other investment funds and not individual stocks or bonds. The investment strategies of these underlying funds are in different asset classes, from equities (stocks) to fixed income assets like bonds, and have different risk/return profiles.

The target date fund’s adviser shifts the target date fund’s assets among the various underlying funds over time, consistent with the fund’s own investment strategy. Typically, this means the target date fund shifts from investing more in stock funds to more in bond funds as the target date nears. The timing of this shifting is called the glide path.

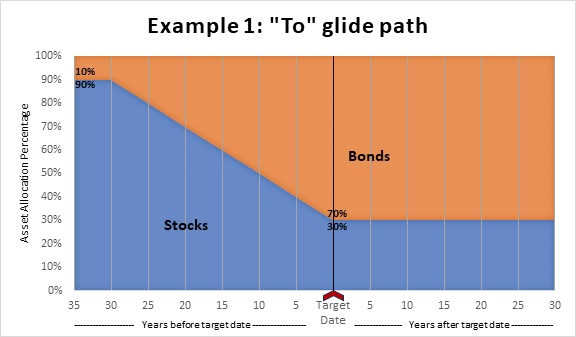

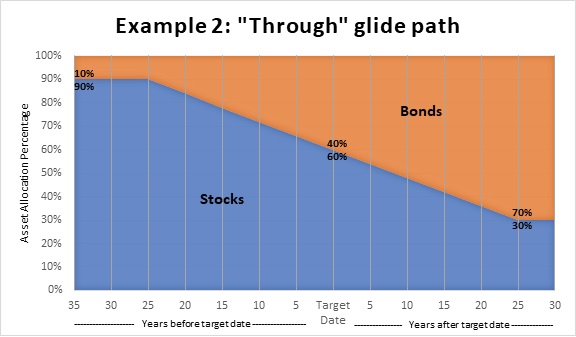

How does the glide path work?

There are two types of glide paths – “to” and “through” the target date.

Funds with a “to” glide path shift their investment mix just until the target date and generally not past that date. See example 1 below.

Funds with a “through” glide path shift their investment mix up to and past the target date. See example 2 below.

Funds with a “to” glide path typically switch to more conservative investments earlier than funds with a “through” glide path. That means that at many points along the glide path a “to” fund is invested in lower return and lower risk investments than a “through” fund.

The type of glide path that is right for you is personal, depending on your comfort with risk and your financial situation.

What are some potential risks of investing in a target date fund?

- Differences in performance. You can’t just rely on the fund’s target date to understand if the investment is right for you. Even target date funds with the same target date often have very different investments and different performance/returns. This is because they have:

- Different investment strategies and risks. Target date funds with the same target date may have different investment strategies and levels of risk. For example, this could mean that the mix of investments all along the glide path may be more conservative or more risky than other funds. These variations may occur before the target date, and also at the target date and after it.

- Different glide paths. Target date funds with the same target date may have different glide paths. This means that the mix of investments gets shifted to more conservative investments at different times or at a different rate.

- Different fees. Target date funds with the same target date may charge different fees. In addition, since a target date fund often invests in other funds, fees may be charged by both the target date fund and the underlying funds. Even small differences in fees can translate into large differences in returns over time.

- No guaranteed retirement income. Target date retirement funds structured as mutual funds and ETFs do not guarantee that you will have sufficient retirement income, or a specific level of retirement income, at or after the target date.

What should I do before investing in a target date fund?

- Carefully read the fund’s available information, including its prospectus and most recent shareholder report. You can get this information by looking at the fund’s filings on the SEC’s EDGAR database, from your investment professional, or directly from the fund free of charge. If you own a target date fund in a retirement plan account, you can also get this information from the plan sponsor and your employer.

- Consider the target date fund’s investment strategy. For example, does the fund invest in a larger percentage of stock than you want at any time along its glide path? Or is it too conservative for your financial goals?

- Understand how the target date fund will change over time. Are you comfortable with the fund’s glide path? In particular, make sure you understand when the fund will reach its most conservative investment mix and whether that works for your plans for the future.

- Understand the fees and expenses you will pay for the fund. Be sure to understand the costs for both the target date fund and for any funds in which the target date fund invests. The fee table in the target date fund’s prospectus will show both. Keep in mind that a fund with high costs must perform better than a low-cost fund to generate the same returns for you. Even small fees can have a large impact on your investment over time.

- Consider your overall asset allocation. When investing in a target date fund for retirement, consider any other investments or sources of retirement income you may have. Carefully examine your overall asset allocation and consider how the target retirement date fund fits in.

- Consider if the fund’s target date is right for you. Target date funds do not eliminate the need for you to decide whether the fund fits your financial situation. Doing so is important both before investing and going forward. For example, even if you plan to retire in 2060, you may decide, based on your investment objectives, tolerance for risk, and other assets, that a 2050, 2070, or other target date retirement fund is more appropriate for you.

This Investor Bulletin represents the views of the staff of the Office of Investor Education and Assistance. It is not a rule, regulation, or statement of the Securities and Exchange Commission (“Commission”). The Commission has neither approved nor disapproved its content. This Bulletin, like all staff statements, has no legal force or effect: it does not alter or amend applicable law, and it creates no new or additional obligations for any person.